-

Audit Financial Services

More security, more trust: Audit services for banks and other financial companies

-

Audit Industry, Services, Institutions

More security, more trust: Audit services for national and international business clients

-

Corporate Tax

National and international tax consulting and planning

-

Individual Tax

Individual Tax

-

Indirect Tax/VAT

Our services in the area of value-added tax

-

Transfer Pricing

Our transfer pricing services.

-

M&A Tax

Advice throughout the transaction and deal cycle

-

Tax Financial Services

Our tax services for financial service providers.

-

Financial Services

Consultancy services that generate real added value for financial service providers.

-

Advisory IT & Digitalisation

Generating security with IT.

-

Forensic Services

Nowadays, the investigation of criminal offences in companies increasingly involves digital data and entire IT systems.

-

Regulatory & Compliance Financial Services

Advisory services in the area of financial market law.

-

Transaction Services / Mergers & Acquisitions

Successfully handling transactions with good advice.

-

Legal Services

Experts in commercial law.

-

Trust Services

We are there for you.

-

Business Risk Services

Sustainable growth for your company.

-

Abacus

Grant Thornton Switzerland Liechtenstein has been an official sales partner of Abacus Business Software since 2020.

-

Accounting Services

We keep accounts for you.

-

Payroll Services

Leave your payroll accounting to us.

-

Real Estate Management

Leave the management of your real estate to us.

-

Apprentices

Career with an apprenticeship?!

BFSA: Agreement between the United Kingdom of Great Britain and Northern Ireland and the Swiss Confederation on Mutual Recognition in Financial Services as of 21 December 2023.

Background

Globally, the BFSA is the first agreement of its kind. Switzerland and the UK had been discussing closer cooperation in their financial markets since 2016 which was reflected by annual financial dialogues. Since the UK officially left the European Union on 31st January 2020, negotiations on a follow-up agreement with Brussels have continued to be difficult and ultimately failed. The UK and Switzerland already had a good level of cooperation within the framework of partial mutual market liberalization. In June 2020, both countries then concluded a Joint Statement at ministerial level in which they confirmed their intention to negotiate an agreement based on the mutual recognition of supervisory and regulatory regimes. In addition, both regulators, the FINMA and FCA, as well as industry associations of both countries were extensively involved.

The BFSA is a treaty under international law which obliges both states to implement the provisions laid down in the BFSA in their respective national laws. It still must be ratified by both parliaments, which is expected to happen in the first quarter of 2024, whereby the referendum requirement must be observed in Switzerland. As is customary and mandatory for international treaties, art. 4 BFSA states that it does not confer any private rights on natural or legal persons. For UK-Swiss cross-border financial services market participants to benefit directly from the BFSA, its provisions and annexes need to be transposed into the national legal systems and could be substantiated by FINMA and FCA with circulars.

Need for action

There will be some time until full implementation into the national laws, currently expected to be in 2024/25. Nevertheless, it is important for market participants interested in leveraging and unlocking the opportunities of the BFSA to strategically analyse and prepare thoroughly for a cross-border market entry under the BFSA right now. Experience has shown that this always requires a lead time. We believe that the organisation’s readiness for such a cross-border market entry could match with the time of enactment of the national laws and regulations corresponding to the BFSA.

Objective

The BFSA is primarily intended to provide the Swiss and UK market participants concerned with legal certainty, predictability, and predictability about the regulation of the other country (art. 2 lit. d. BFSA). The core element is the mutual recognition of each domestic regulatory and supervisory framework (art. 8, 7 and 9 BFSA and its sectoral annexes). For the sectors governed by the BFSA, both countries assume that the regulation and supervision of the other country will achieve equivalent results in terms of financial stability, market integrity and investor and consumer protection within the framework of this agreement (outcomes-based mutual recognition of domestic laws and regulations; art. 2 lit. d., 8 BFSA). This will be underpinned by close regulatory cooperation (art. 13 et seq. BFSA). In principle, mutual recognition applies as a base line within the framework of the BFSA. This is specified and partially watered down in its sectoral annexes. Automatic recognition is not provided for all sectors, principle only for central counterparties and investment services regarding activities of financial intermediaries from Switzerland into the United Kingdom and for central counterparties, insurers, and investment services from the United Kingdom into Switzerland. Even here, recognition is softened based on specific definitions of covered services and clients special as well as special conditions.

Covered sectors

The BFSA covers the following five sectors of:

- asset management;

- banking;

- financial market infrastructures;

- insurance and

- investment management embracing banks, securities firms, fund management companies, managers of collective assets and portfolio managers.

In the BFSA’s sectoral annexes definitions of covered financial services, financial instruments and covered clients further tunnel the sectors and business areas which adhere to domestic law provisions or deference. We assume that also Swiss-UK cross-border M&A as well as private equity transactions will be fostered.

Mechanisms for mutual recognition and deference

Conceptually, the BFSA functions in such a way that the market segments including their covered services and clients are assigned to three different levels of recognition:

- Recognition as a general principle of the BFSA, which means that the financial intermediaries are mutually and reciprocally recognised, i.e. they do not require a foreign license from the host country’s regulator for cross-border activities into the host country from their home country, and vice versa (mutual regulatory recognition).

- Swiss and UK financial intermediates may operate in the host country largely in accordance with the regulatory and supervisory rules that apply in their home country (deference).

- Operating under the regulatory recognition, whereby operations may only be conducted in compliance with the domestic law of the host country, as being specified under the BFSA (domestic law)

- Other arrangements (other arrangements) and

- Conditions to the above (conditional provisions).

This cascade of recognition and deference enables to apply domestic law to specific sectors in the interest of financial stability, market integrity and investor protection where this is more appropriate, for example regarding the riskiness of the transactions. When it comes to deference, being granted e.g. for highly standardized wholesale or professional counterparty insurance, the deference, in addition to regulatory recognition, allows the target operating model of the country of home regulation to be used for the cross-border business. In this respect, a financial intermediary can operate within the framework of the BFSA in the host country under nearly the same operational processes and plan with comparable operational risks, as it can operate in its home state.

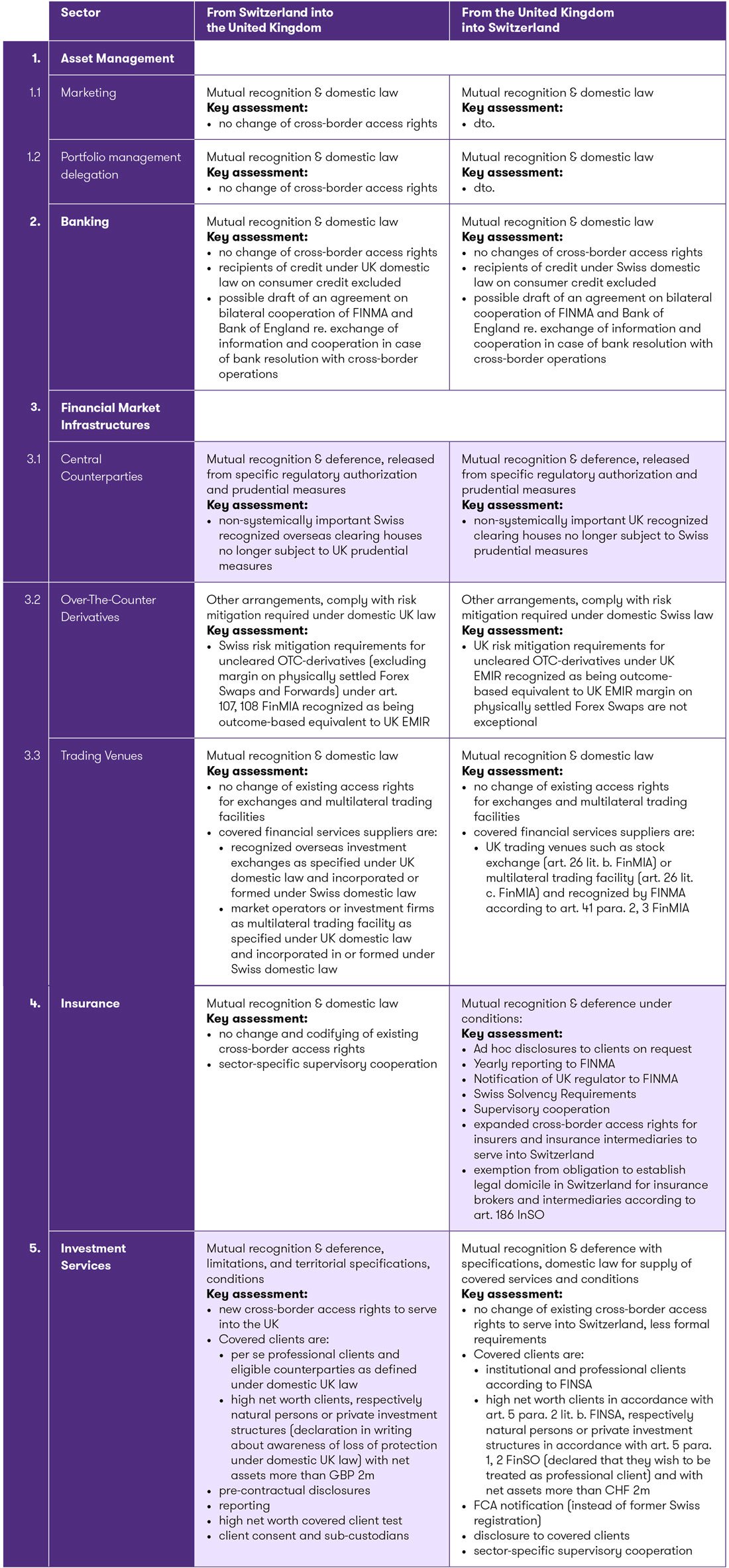

The requirements across the relevant sectors are as follows, whereby we do not take the detailed covered services and client specifications into account for this non-exhaustive mapping including a first assessment on the most important benefits:

The table shows that the full exemption to serve in the other country under the license granted by the home country, is mostly modified by the domestic regulatory and supervisory concepts, demanding additional domestic law requirements and further conditions. The concept of deference applies in principle only for the sector of financial market infrastructures/central counterparties and at most for the investment services while specific limitations and partly Swiss domestic law applies for UK firms serving into Switzerland. Covering the financial market infrastructures both countries entered a Side Letter clarifying that they would like to enter into closer cooperation also for credit rating agencies, trade repositories, OTC-derivatives clearing obligations and set-up OTC-derivatives intragroup exemptions for domestic firms what should be prioritised in the further development of the BFSA.

The BFSA is subject to a revolving review and both regulators also strive for regulatory and supervisory innovations (art. 2 lit. c. BFSA). This is intended both to flank the principle of outcomes-based mutual recognition and deference as well as to sharpen mutual trust and understanding between the FINMA and FCA. Above all, cooperation, mutual information, and the establishment of tools for managing disagreements and safeguards within the BFSA (e.g. art. 14 et seq., 20, 24) serve to create a dynamic and trusting regulatory and supervisory basis.

Domestic law implications

Much more important for market participants is the question which detail domestic law must be applied if a deference is not applicable or additional conditions effectively inbound specific domestic rules. It is expected that particularly but not exclusively the following primary and secondary laws will be amended along the BFSA and will then govern each domestic law framework for Swiss and UK cross-border business activities.

UK key domestic law for Swiss financial intermediaries

From a Swiss perspective, the Financial Conduct Authority’s Conduct of Business rules must be complied with, as well as requirements regarding financial promotions set out in the Financial Services and Markets Act 2000.

The UK’s Conduct of Business rules have been developed based on MIFID I and II provisions, however they go further in some areas, notably with expanded requirements applying to the process by which the suitability of any advice being provided must be assessed and/or the appropriateness of financial products being sold. There is also the possibility of the activity being captured under the new UK Consumer Duty obligations if a service or product being provided to a financial business in the UK might form part of a service to an end retail client of that business. Swiss intermediaries that have not been granted a deferral must be prepared to implement significantly stricter regulations compared to MiFID II (provided they have implemented MiFID II risk-based) and FINMIA (FinfraG), FINSA (FIDLEG). In addition, the UK-anti money laundering and antifinancial crime laws and regulations must be observed and complied with UK MLR, JMLSG Guidance.

UK key domestic law for Swiss financial intermediariesey Opportunities for Swiss intermediaries: entering the UK market with investment management services

From a UK perspective, particularly and not conclusive especially the following Swiss laws and regulations must be observed, implemented and complied with if the Swiss market should be served out of the UK: the BA (BankG), FINMIA (FinfraG), FINSA (FIDLEG), FinSO (FIDLEV), ISA (VAG), InSO (AVO), InSO-FINMA. In addition, the Swiss anti-money laundering and anti-financial crime laws and regulations must be considered including the Swiss banking client confidentiality.

Key opportunities of the BFSA for Swiss and UK financial intermediaries

All in all, the BFSA offers the greatest opportunities for Swiss investment management services intermediaries and UK insurers, independent insurance brokers and insurance services providers, to operate relatively cheaply in the other country. This does not mean that there are fewer opportunities for the other sectors covered by the BFSA. The concept of deference does not apply to the other sectors, which means that additional effort is required to implement domestic law in the operational models.

Key Opportunities for Swiss intermediaries: entering the UK market with investment management services

The BFSA is of particular interest to financial intermediaries active in the investment management-business. Here, the UK complies with the Swiss regulatory and supervisory framework by way of a deference. There is therefore enormous potential in this sector for Swiss banks, securities firms, fund management companies, managers of collective assets or asset managers to become active in the UK from Switzerland at relatively low cost based on the Swiss supervisory and regulatory framework allowing them to operate from a regulatory and supervision perspective on the existing target operating models which need to be aligned, for example, with the relevant UK civil, banking client secrecy and data protection laws and regulations.

Key Opportunities for UK intermediaries: entering the Swiss market with insurance services

The BFSA offers great potential for UK insurers, independent insurance brokerage firms and other insurance intermediaries providing auxiliary insurance services (the latter has been confirmed by a Side Letter as of 21 December 2023) with a legal seat in the UK to enter the Swiss market. According to independent insurance brokers, Switzerland makes an exception exclusively for UK firms from the obligation to establish a business in accordance with the revised Swiss Insurance Supervision Act (ISA, VAG), which has been in force since 1 January 2024.

Opportunities for intermediaries already licensed in the respective other country

The question arises as to what impact the BFSA will have on providers that are already fully or partly (e.g. as a branch) licensed in the other country and are already doing business there. Only those providers which do not have a license in the respective host country can benefit from the BFSA, respectively the rules provided therein once being transformed into the national financial services laws and regulations.

After all, a reorganization of a business unit that is already separately licensed and operating the business in a host country if it appears operationally more efficient to offer the services from the home country. Specifically, this would involve downgrading to and lining-up into the home country-based parent company or, depending on the legal and operational structure, to another home country carrier which is licensed under the home country’s regulation. For service providers without direct contact to the client however, the downgrading of previously separately regulated subsidiaries or branch offices could be worth considering for reasons of efficiency and aligned intra-group service level arrangements. In our view, there may be interesting opportunities for optimized operations that can significantly reduce regulatory cost. We recommend first analysing the legal, regulatory, operational and tax conditions in detail before you start a delineation project.

Next steps

As soon as the two parliaments have ratified the BFSA and the corresponding referendum has been adopted in Switzerland, both countries will begin to transpose the BFSA into their national laws and regulations. It is currently discussed that this will happen by 2025. Market participants will then be able to benefit directly from the provisions of the BFSA, which will then have been transformed into the national laws and regulations of the UK and Switzerland.

However, it can also be seen that both countries are still much more cautious about various sectors and that the BFSA offers clear advantages overall but is not yet the “big hit” for fully integrated and internalised bilateral financial markets in both countries. Both states emphasised that the BFSA is initially a starting point and that they, with the active involvement of the FINMA and FCA, would like to develop the BFSA further. There is still some time left for strategic clarifications and preparations for cross-border market entry, but if there is interest in serving clients cross-border, time should be used now to be ready when the BFSA will be transposed into the national laws.

|

How Grant Thornton Switzerland and UK can jointly support you: At Grant Thornton we have formed a joint Swiss-UK expert team covering all relevant disciplines for establishing and safeguarding Swiss-UK cross-border activities. We are keen to support you in the following key areas and to unlock your cross-border potential.

|

Contacts

|

Dr. Sebastian Neufang |

|

Felix M. Huber |

|

David Morrey |

|

Paul Garbutt |